📘 SI BONE INC (SIBN) — Investment Overview

🧩 Business Model Overview

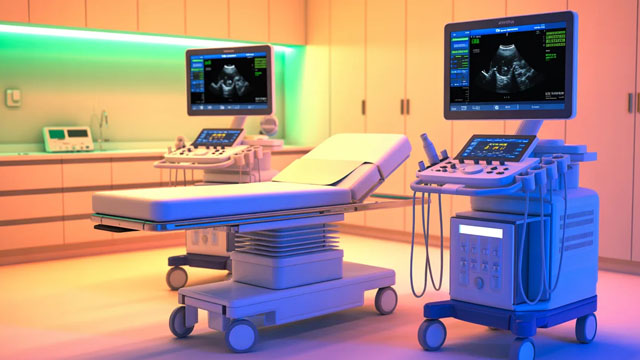

SI-BONE sells a robotics-enabled surgical platform designed to guide surgeons during sacroiliac (SI) joint fusion procedures, paired with proprietary, physician-implanted consumables (fusion implants and related products). The economic engine is an “installed base + consumables” model: once a hospital, surgeon group, or surgical center adopts the system, ongoing procedures create recurring demand for the company’s compatible implant solutions. Adoption is reinforced by procedural standardization, training and workflow integration, and the practical learning curve associated with robotic-assisted SI joint surgery.💰 Revenue Streams & Monetisation Model

Revenue is driven by two main components:- Systems revenue: upfront sales of the robotic platform and related equipment for surgery.

- Consumables revenue: recurring sales of proprietary implants used in each procedure.

🧠 Competitive Advantages & Market Positioning

SI-BONE’s core moat is switching costs created by clinical workflow + proprietary procedural ecosystem, rather than broad, generalized robotics coverage. Once a provider has trained teams and integrated a robotic-assisted SI fusion pathway, switching to another approach can be operationally disruptive (system training, surgeon technique familiarization, inventory alignment, and institutional preference for established outcomes). Key differentiators:- High procedural specificity: focus on SI joint fusion enables deeper product/tested workflow alignment versus generalized navigation robotics.

- Proprietary compatibility: implant solutions are designed to work with SI-BONE’s system-driven workflow, creating practical dependency on the company’s consumables.

- Installed base effects: growing case volume strengthens surgeon confidence, referral patterns, and institutional willingness to schedule more procedures.

- Medtronic (Mazor X/ROSA ecosystem): broader robotics and navigation presence across orthopedic/spine workflows. Medtronic’s advantage is breadth and distribution; SI-BONE’s advantage is focused depth in SI joint fusion.

- Globus Medical (navigation/robotics-adjacent solutions such as ExcelsiusGPS): established spine platform presence. Globus can offer an integrated spine portfolio; SI-BONE competes by emphasizing SI-specific robotics-enabled fusion workflows and proprietary consumables.

- Brainlab (navigation/robotics-enabled planning): strength in digital planning and navigation across multiple surgical indications. SI-BONE competes via a narrower but more procedure-specific ecosystem, aiming for repeatability in SI fusion care pathways.

🚀 Multi-Year Growth Drivers

A 5–10 year growth framework is supported by structural drivers:- Secular shift toward minimally invasive, image/robot-guided procedures: robotics-enabled guidance can reduce variability and supports repeatable surgical execution, supporting a gradual substitution away from more invasive approaches.

- Expansion of treatable addressable population: better diagnostic refinement and broader willingness to pursue SI joint fusion can increase procedure incidence and repeat-treatment conversion.

- Installed base maturation: the path to durable growth depends on increasing procedure frequency per installed system and improving “attach” of proprietary consumables.

- International expansion: exporting an established procedure pathway can extend market reach where regulatory clearance, reimbursement, and surgeon training footprints scale over time.

- Portfolio development within the SI fusion ecosystem: incremental product improvements and procedure pathway refinements can increase average revenue per case and improve clinical adoption.

⚠ Risk Factors to Monitor

- Regulatory and clinical validation risk: product clearances and label expansions can influence adoption pace; clinical evidence and surgeon outcomes remain central to payer and provider acceptance.

- Adoption curve and reimbursement dynamics: growth depends on sustained hospital utilization, training throughput, and coding/reimbursement structures that support procedure economics.

- Technological substitution: navigation, imaging, and robotic capabilities from larger platform players can compress differentiation unless SI-BONE maintains a compelling procedure-specific value proposition.

- Manufacturing and quality systems: as consumable volume scales, quality management and supply continuity are critical; disruptions can impair revenue and regulatory standing.

- Concentration risk: dependence on SI joint fusion as the central revenue theme can make the company sensitive to changes in clinical practice patterns or competitive penetration within SI fusion.

📊 Valuation & Market View

The market typically values medtech growth companies using a blend of revenue multiple frameworks (often anchored by P/S) and cash-flow or earnings power expectations (EV/EBITDA or EV/FCF once operating leverage is evident). The valuation “drivers” that tend to move the needle for an installed-base + consumables model include:- Installed base growth and utilization (systems placements with path to higher case frequency)

- Consumables attach rate and evidence of durable ordering per procedure

- Gross margin trajectory as consumables scale and manufacturing utilization improves

- Operating leverage from sales productivity, service efficiency, and R&D spend discipline

- Balance-sheet strength and cash runway, given commercialization and ongoing product development needs

🔍 Investment Takeaway

SI-BONE’s long-term thesis rests on a procedure-specific installed base model that can create durable switching costs for providers: adopting SI-BONE’s robotic-guided SI fusion pathway typically leads to ongoing dependence on proprietary consumables and entrenched surgical workflow habits. Over a multi-year horizon, growth depends on sustained adoption of robotic-assisted SI fusion, maturation of the installed base into higher procedure frequency, and continued differentiation versus broader spine robotics and navigation competitors. The investment case is strongest when evidence points to durable consumables growth, improving operating leverage, and clinical and reimbursement momentum for SI joint fusion.⚠ AI-generated — informational only. Validate using filings before investing.