📘 CHART INDUSTRIES INC (GTLS) — Investment Overview

🧩 Business Model Overview

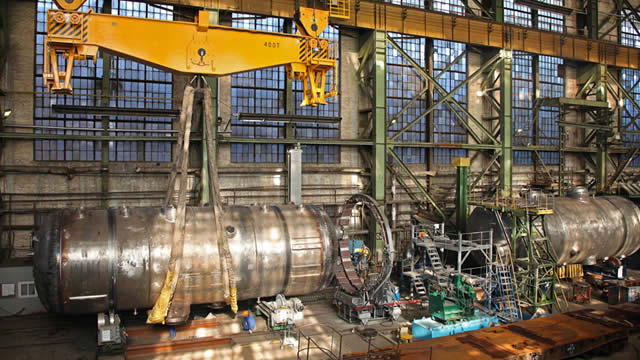

Chart Industries designs, manufactures, and services cryogenic and process equipment used to produce, store, and transport low-temperature gases. The company’s “how it works” centers on matching engineered systems—delivering strict thermal performance and safety requirements—to the operational needs of upstream and midstream gas customers, LNG operators, and industrial gas producers.

Revenue is supported by (1) project and equipment delivery tied to capacity buildouts, and (2) lifecycle support—parts, upgrades, field services, and service-driven relationships maintained after installation. This structure creates an installed base that behaves differently from pure “one-and-done” capital goods vendors.

💰 Revenue Streams & Monetisation Model

Chart monetizes through a mix of equipment sales and aftermarket/service revenue:

- Systems and equipment sales (more transactional): Deliveries of engineered cryogenic systems and related components sold to customers building or expanding gas processing, LNG, and industrial gas infrastructure.

- Aftermarket and service (more recurring): Ongoing revenue streams from spare parts, maintenance, refurbishments, and service programs that extend the operating life and reliability of installed equipment.

- Upgrades and replacement cycles: Periodic reconditioning and modernization work driven by fleet age, operational performance targets, and compliance requirements.

Margin structure typically reflects a higher-margin tilt toward services/aftermarket versus commoditized manufacturing. For equipment projects, gross margin depends on engineering content, manufacturing execution, and procurement discipline; for service, margin resilience tends to improve with customer stickiness and backlog visibility from the installed base.

🧠 Competitive Advantages & Market Positioning

Chart’s competitive strength is rooted in hard technical requirements, customer qualification, and lifecycle service relationships—factors that support defensible switching costs.

- Switching costs (installed base & qualification): Cryogenic systems require long qualification cycles, tight performance tolerances, and safety-critical integration. Once equipment is installed and certified, customers often prefer using established service partners for parts, repair procedures, and reliability-driven maintenance.

- Engineering and application expertise (intangible capability): The business relies on specialist know-how in thermal management, reliability engineering, and system integration for gas handling at cryogenic temperatures.

- Aftermarket penetration leverage (sticky service ecosystem): A broad installed fleet supports recurring service demand, creating a stabilizing offset to equipment-cycle volatility.

Competitive benchmarking:

- Howden (industrial process and compressors/thermal systems): More frequently associated with broader rotating equipment and process engineering; Chart’s differentiation concentrates on cryogenic system specialization and lifecycle support for low-temperature gas applications.

- Alfa Laval (heat transfer and separation technologies): Strong presence in thermal/heat exchange solutions; Chart’s focus emphasizes cryogenic performance and end-to-end cryogenic equipment needs for LNG and gas processing fleets, where service continuity can matter materially.

- Baker Hughes (oilfield and process equipment/services): Diversified across upstream/midstream assets; Chart operates more narrowly in cryogenic and LNG-adjacent equipment/services, which can translate into deeper installed-base expertise.

In practice, Chart competes where deep cryogenic know-how and lifecycle service coverage are decisive, rather than where general-purpose thermal equipment or commoditized fabrication dominates.

🚀 Multi-Year Growth Drivers

Over a 5–10 year horizon, demand is supported by structural infrastructure and energy-transition-related buildouts:

- LNG and gas processing expansion: Ongoing development and debottlenecking of LNG liquefaction, storage, and transfer systems sustain equipment replacement and upgrade needs.

- Marine and port LNG infrastructure: Growth in LNG as a marine fuel drives demand for cryogenic handling and terminal-related equipment, along with service for operational continuity.

- Industrial decarbonization pathways via hydrogen: Hydrogen supply chains require cryogenic or otherwise low-temperature handling solutions in certain routes; as projects scale, specialized equipment and reliability-focused service demand tend to follow.

- Fleet lifecycle modernization: Older installed equipment supports upgrades, reconditioning, and compliance-driven improvements—creating a durable aftermarket component.

These drivers expand total addressable activity in both “build” and “support” cycles. Importantly, Chart’s installed-base service model can convert a portion of growth in infrastructure utilization into recurring revenue visibility.

⚠ Risk Factors to Monitor

- Capital-cycle and project timing risk: Equipment-heavy revenue can be exposed to the timing of customer capex decisions across LNG, industrial gas, and hydrogen supply chains.

- Execution and delivery risk: Cryogenic systems are complex; delays, cost overruns, or warranty/performance issues can compress margins.

- Commodity and input cost exposure: Procurement cycles for materials and components can impact manufacturing economics.

- Competitive pressure in engineered process equipment: Large industrial peers can compete for parts of value chains where bids emphasize price or general capability rather than cryogenic specialization.

- Regulatory and safety compliance burden: Changes in safety standards and permitting requirements for LNG/hydrogen handling can affect design requirements and qualification pathways.

- Technology-route uncertainty: Hydrogen and low-temperature processing adoption may favor different technical pathways; equipment demand remains tied to project choices and timelines.

📊 Valuation & Market View

The market typically values Chart-like industrial equipment/service firms using a blend of:

- EV/EBITDA and operating margin expectations: Reflects the cyclical nature of equipment delivery and the importance of sustainable margins.

- Revenue quality metrics (mix and aftermarket share): A higher proportion of service/aftermarket revenue generally improves earnings durability and downside protection versus pure capex cycles.

- Order book/backlog conversion and service pipeline: Moving from awarded projects to delivered revenue drives how investors underwrite earnings power.

Key valuation drivers usually center on service penetration, normalized operating margins, and the sustainability of end-market capex programs for LNG and low-temperature gas infrastructure.

🔍 Investment Takeaway

Chart Industries offers a specialized cryogenic equipment and service platform with structurally advantaged customer stickiness. The moat is supported less by advertising or brand and more by engineering qualification barriers, safety-critical performance requirements, and an installed-base service ecosystem that can provide earnings resilience through industry cycles. For investors, the long-term thesis rests on continued LNG and low-temperature infrastructure investment, coupled with lifecycle modernization and aftermarket growth that converts infrastructure buildouts into recurring service economics.

⚠ AI-generated — informational only. Validate using filings before investing.