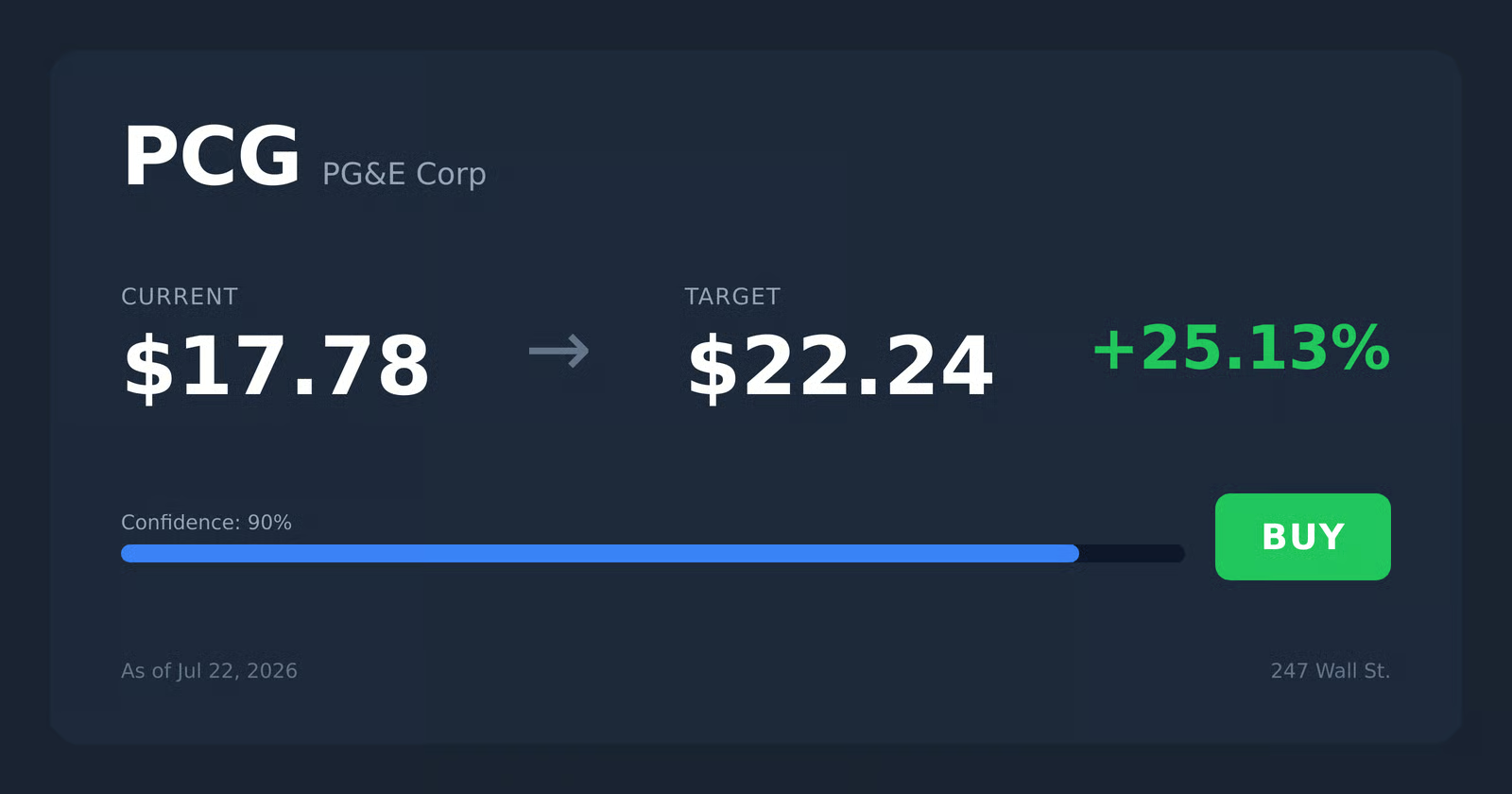

📘 PG&E CORP (PCG) — Investment Overview

🧩 Business Model Overview

PG&E operates regulated utility networks that deliver essential energy services within defined geographic service territories in Northern and Central California. The value chain is straightforward: (1) utilities acquire and transmit energy (electricity and natural gas) through long-lived infrastructure, (2) they distribute that energy to end customers, and (3) they maintain safety, reliability, and compliance via ongoing inspection, operational controls, and capital expenditures.

Customer “stickiness” is structural. Residential and commercial customers cannot practically switch away from the local electric and gas distribution network because the utility’s poles, wires, pipelines, and operating permits are fixed to the geography. This creates high switching costs at the customer level and supports predictable service demand, even when consumption patterns fluctuate.

💰 Revenue Streams & Monetisation Model

PG&E’s monetisation is dominated by regulated tariff mechanisms tied to its investments in the grid and its cost-to-serve. The core revenue logic is “rate base economics”: the utility earns an allowed return on prudently spent capital and recovers operating costs through approved rates.

- Distribution and transmission (electric): Revenue primarily reflects grid usage and regulatory recovery of operational expenses plus an allowed return on the electric network.

- Gas distribution: Revenue reflects serving local gas demand and the costs of operating and maintaining gas pipelines, including safety and compliance programs.

- Regulatory recovery of capital and operating costs: Large categories of spending (reliability upgrades, wildfire hardening, system modernization) are monetised through regulatory rate approvals and mechanisms that can offset earnings volatility.

Margin drivers are less about competitive pricing power and more about (1) regulatory approval of the cost of capital and the prudency of spending, (2) the efficiency of executing capital programs, and (3) the stability of allowed recovery versus weather- and volume-driven operating variability.

🧠 Competitive Advantages & Market Positioning

PG&E’s moat is primarily geographic and regulatory: long-lived network assets located within exclusive service territories, backed by permitting, franchise rights, and a regulatory regime that remunerates the utility for providing reliability and safety. The practical effect is that competitors cannot replicate the network fast enough to challenge market share at the retail level.

Key moat characteristics:

- Switching Costs (customer-level): End users are effectively tied to the local electric and gas distribution infrastructure.

- Geographic Cost Advantage (asset locality): The company’s network spans dense, defined service territories; duplicating poles, wires, and pipeline corridors is capital- and permitting-intensive.

- Regulatory Moat: Earnings power is shaped by tariff structures, recovery mechanisms, and allowed returns—competitors lack the same approved service footprint.

Competitive benchmarking (industry peers): PG&E is a California investor-owned utility with electric and gas distribution/transmission exposure. Primary peers include:

- Southern California Edison (SCE) — Edison International (electric utility focus in a neighboring California territory)

- San Diego Gas & Electric (SDG&E) — Sempra Energy (electric and gas utility operations in another California territory)

- Duke Energy (regulated utility model across broader U.S. geographies, with differing regulatory and wildfire/weather risk profiles)

Compared with these rivals, PG&E’s competitive positioning is shaped by the specific California operating environment—particularly wildfire risk management and the pace and scope of grid hardening and compliance investments. While the regulated-utility business model is shared, the risk and capital cadence are more idiosyncratic to the Northern/Central California footprint.

🚀 Multi-Year Growth Drivers

Over a 5–10 year horizon, growth is driven by the need to maintain and modernize critical infrastructure while integrating evolving load patterns. In regulated utilities, “growth” typically manifests through rate base expansion and reliability-linked capital investment rather than rapid customer acquisition.

- Grid modernization and reliability hardening: Sustained capital programs aimed at reducing outage frequency and improving system resiliency support long-term earnings visibility subject to regulatory prudency review.

- Electrification and load growth mix: Technology and policy tailwinds shift energy usage toward electricity, increasing the relevance of distribution capacity, interconnection, and system planning.

- Renewable integration and power quality: As generation mix evolves, the grid requires upgrades in control systems, distribution management, and transmission/distribution interdependencies.

- Gas system safety and integrity: Ongoing pipeline inspection, replacement, and compliance investments protect the asset base that underpins stable gas distribution service.

The total addressable “opportunity” is largely represented by the regulated capital and operating programs required to keep the grid safe, reliable, and compliant—capital intensity that converts into earnings when regulatory outcomes are favorable.

⚠ Risk Factors to Monitor

- Regulatory approval risk: Earnings depend on prudency determinations, cost recovery mechanisms, and the treatment of risk items in tariff proceedings. Adverse regulatory outcomes can compress allowed returns or delay recovery.

- Wildfire and liability exposure: The durability of balance sheet protections, claims management, and reserve frameworks materially affects investor confidence and financing flexibility.

- Capital intensity and execution risk: Large infrastructure programs introduce schedule, cost, and contractor performance risks. Execution problems can raise regulatory scrutiny and reduce the margin of safety.

- Financing and credit profile: Regulated utilities require ongoing capital; cost of capital and credit conditions can influence the effectiveness of capital plans and the stability of funding sources.

- Operational and cybersecurity risk: Grid control systems and operational technology create targets for cyber events; reliability interruptions can also create downstream regulatory penalties or reputational damage.

- Weather and demand volatility: Extreme heat, wildfire conditions, and consumption swings can pressure operating costs, outage rates, and volume-related metrics.

📊 Valuation & Market View

The market typically values regulated utilities through a lens that differs from classic growth equities. Traditional multiples (such as EV/EBITDA or price-to-book) are supplemented by the market’s expectations for:

- Allowed return on rate base: Confidence in the cost of capital and the stability of regulatory outcomes supports higher valuation multiples.

- Rate base growth quality: Capital programs that are demonstrably prudent and reliably recoverable are valued more favorably than discretionary or contested spending.

- Risk premium: Wildfire/liability uncertainty and regulatory friction can raise the implied risk premium, lowering valuation despite durable underlying demand.

- Cash flow durability: The ability to convert regulated earnings into predictable cash flows influences enterprise value and credit-sensitive valuation metrics.

Catalysts that move valuation are usually structural rather than cyclical: progress on regulatory clarity, de-risking of liability exposure, and successful execution of grid modernization programs within approved frameworks.

🔍 Investment Takeaway

PG&E’s long-term thesis rests on a structural utility franchise: fixed geographic service territory, high customer switching costs, and a regulatory model that can monetize prudently executed grid investment. The investment case is strongest when regulatory outcomes support recovery of capital and operating costs, and when wildfire and liability risks are managed in a way that preserves cash flow durability and credit resilience. The key determinant of equity performance is not competitive displacement, but the balance of (1) rate base growth and execution quality versus (2) regulatory friction and liability risk.

⚠ AI-generated — informational only. Validate using filings before investing.