QXO, Inc. (QXO) Market Cap

QXO, Inc. has a market capitalization of $9.64B.

Price: $13.30

▼ -0.16 (-1.19%)

Market Cap: 9.64B

NYSE · time unavailable

CEO: Bradley S. Jacobs

Sector: Industrials

Industry: Industrial - Distribution

IPO Date: 2012-04-17

Website: https://www.qxo.com

QXO, Inc. (QXO) - Company Information

Market Cap: 9.64B|Sector: Industrials

Company Profile

QXO, Inc. is a publicly traded distributor of roofing, waterproofing and complementary building products in the United States. It plans to become tech-enabled in the building products distribution industry and generate outsized value for shareholders. The company was founded on October 3, 2002, and is headquartered in Greenwich, CT.

Analyst Sentiment

From 14 Active Polls

1Y Forecast: $27.60

▲ +107.5% Potential Upside

Consensus Target Metrics

Low Bound

$18

Median

$30

High Bound

$32

Average

$28

Price & Moving Averages

🎯 Wall Street Analyst Intelligence Report

1-Year structural target targets, chart projections, and sentiment maps.

Consensus Trend Projection

Trailing closures vs. 12-month metrics map.

Analyst Vote Distribution

Aggregate institutional coverage sentiment weights.

📊 Historical Valuation Multiples

Real-time Trailing Twelve Month (TTM) momentum side-by-side with discrete quarterly metrics.

| Fiscal Quarter | TTM | Q1 2026 | Q4 2025 | Q3 2025 | Q2 2025 | Q1 2025 | Q4 2024 | Q3 2024 | Q2 2024 |

|---|---|---|---|---|---|---|---|---|---|

| Period Ending | Trailing 12M | Mar 31, 2026 | Dec 31, 2025 | Sep 30, 2025 | Jun 30, 2025 | Mar 31, 2025 | Dec 31, 2024 | Sep 30, 2024 | Jun 30, 2024 |

| Market Cap ($M) | 9,644 | 14,456 | 13,821 | 13,634 | 12,164 | 6,112 | 7,178 | 5,658 | 20,670 |

| Enterprise Value ($M) | 10,501 | 15,312 | 15,374 | 15,281 | 14,000 | 1,031 | 2,110 | 622 | 19,701 |

| Price to Earnings Ratio (P/E) | -14.62 | -13.87 | -28.37 | -19.85 | -35.90 | -111.35 | -160.28 | -262.83 | -1.57 |

| Price/Earnings-to-Growth Ratio (PEG) | — | — | — | -0.46 | -0.00 | — | -13.28 | — | -3.54 |

| Price to Sales Ratio (P/S) | 1.13 | 8.36 | 6.30 | 5.00 | 6.38 | 452.50 | 486.86 | 430.14 | 1425.54 |

| Price to Book Ratio (P/B) | 0.97 | 1.42 | 1.42 | 1.39 | 1.23 | 1.21 | 1.42 | 1.12 | 21.28 |

| Price to Free Cash Flow Ratio (P/FCF) | 49.31 | 300.55 | 87.37 | 74.75 | -62.99 | 171.22 | 133.11 | 179.04 | -19686.24 |

| Enterprise Value to Sales (EV/Sales) | — | 8.85 | 7.01 | 5.60 | 7.34 | 76.34 | 143.11 | 47.29 | 1358.71 |

| Enterprise Value to EBITDA (EV/EBITDA) | 76.20 | -256.92 | 176.31 | 73.01 | -141.27 | 58.77 | 23.69 | 26.57 | -41389.25 |

| Debt to Equity Ratio | 6.21 | 0.38 | 0.40 | 0.40 | 0.42 | 0.00 | 0.00 | 0.00 | 0.00 |

📰 Market News & Coverage

15 Stories AvailableReal-time institutional reporting and market updates for QXO.

3 Retirement Stocks I Want To Own For The Next 20 Years

I anchor my long-term retirement strategy on QXO, REXR, and CME, blending growth, income, and wide-moat resilience. QXO is a high-conviction, founder-led housing distribution play with significant upside potential if housing markets recover. REXR offers a 4.5% yield and turnaround potential as Southern California industrial rents stabilize and absorption rebounds.

QXO, Inc. $QXO Shares Sold by California Public Employees Retirement System

California Public Employees Retirement System trimmed its position in QXO, Inc. (NYSE: QXO) by 22.4% in the undefined quarter, according to the company in its most recent disclosure with the Securities and Exchange Commission. The fund owned 796,397 shares of the company's stock after selling 229,719 shares during the quarter. California Public Employees

Alger Capital Appreciation Fund Q2 2026 Portfolio Update

Class A shares of the Alger Capital Appreciation Fund outperformed the Russell 1000 Growth Index during the second quarter of 2026. Nebius Group has positioned itself as a leading next-generation cloud provider purpose-built for machine learning and high-performance computing workloads. Netflix's shares detracted from performance during the quarter despite first-quarter results that beat on revenue and held full-year guidance intact.

QXO: Trusting The Brad Jacobs Playbook For Long-Term Returns

A short-term focus on housing weakness has driven QXO to be undervalued if it can continue its consolidation of the building products distribution market. Strong CEO in Brad Jacobs, who has a superb track record of industry consolidation with previous ventures: United Rentals and XPO Inc., both returned >6,000% since their IPOs. I rate QXO a "Buy" at $15 or below, driven by strong EBITDA growth associated with the official closing of the TopBuild acquisition on July 1, 2026.

QXO Just Finished Building The Machine, And The Market Sold The News

QXO, Inc. has completed its $17B TopBuild acquisition, creating an $18B revenue platform with nationwide reach. Despite integration risks and near-term losses, QXO trades below its acquisition price for TopBuild, presenting a compelling long-term value opportunity. Management targets $4B organic EBITDA by 2030, with a clear blueprint for procurement synergies, technology rollout, and cross-selling across its diversified portfolio.

NTTYY vs. QXO: Which Stock Is the Better Value Option?

Investors interested in stocks from the Technology Services sector have probably already heard of NTT (NTTYY) and QXO, Inc. (QXO). But which of these two stocks is more attractive to value investors?

NYSE Content Update: Vurvey Labs Launched 'Populations 2.0' AI Platform

NYSE issues a pre-market daily advisory direct from the trading floor. NEW YORK, July 8, 2026 /PRNewswire/ -- The New York Stock Exchange (NYSE) provides a daily pre-market update directly from the NYSE Trading Floor.

A Look at QXO Inc (QXO) After 3.5% Decline -- GF Value $16.50 vs Price $15.25

On July 07, 2026, QXO Inc (QXO) shares fell 3.5% today, trading at $15.25. This decline is part of a broader trend, with the stock down 20.9% year-to-date and 2

QXO Completes Acquisition of TopBuild

GREENWICH, Conn.--(BUSINESS WIRE)--QXO, Inc. (NYSE: QXO) today announced it has closed its previously disclosed acquisition of TopBuild Corp. The transaction significantly expands QXO's scale and capabilities across the building products value chain. QXO now holds leadership positions in key building product categories in North America: #1 in insulation #2 in roofing #1 in waterproofing #1 or #2 in the lumber and building materials sector, in key geographies served The company also announced th.

Stock Market Today, June 30: QXO Falls After TopBuild Merger-Election Results Show Most Shareholders Opt for Cash

Expand NYSE: QXO QXO Today's Change (-3.03%) $-0.54 Current Price $17.28 Key Data Points Market Cap $13B Day's Range $16.33 - $18.60 52wk Range $14.75 - $27.61 Volume 89.9M Avg Vol 16.6M Gross Margin 16.24% QXO (QXO 3.03%), a roofing and building products distributor, closed at $17.28, down 3.03%. Merger-election results for TopBuild showed most shareholders choosing cash, and investors are watching the expected July 1 close.Trading volume reached 87.3 million shares, more than five times the three-month average of 16.3 million shares.

QXO Announces the Expiration and Final Results of Cash Tender Offers and Consent Solicitations for Any and All of TopBuild Corp.'s 4.125% Senior Notes due 2032 and 5.625% Senior Notes due 2034

GREENWICH, Conn.--(BUSINESS WIRE)--QXO, Inc. (“QXO”) (NYSE: QXO) announced today the expiration and final results of the previously announced tender offers and consent solicitations (collectively, the “Tender Offers and Consent Solicitations”) by QXO's wholly-owned subsidiary, Titanium MergerCo, Inc., a Delaware corporation (the “Company”), for the (i) $500.0 million aggregate principal amount of outstanding 4.125% Senior Notes due 2032 (the “2032 Notes”) and (ii) $750.0 million aggregate princ.

QXO and TopBuild Announce Stockholder Election Results for Merger Consideration

GREENWICH, Conn. & DAYTONA BEACH, Fla.--(BUSINESS WIRE)--QXO, Inc. (NYSE: QXO) (“QXO”) and TopBuild Corp. (NYSE: BLD) (“TopBuild”) today announced the results of TopBuild stockholders' elections regarding the form of merger consideration (the “Merger Consideration”) to be received in connection with QXO's acquisition of TopBuild (the “Transaction”). As previously disclosed, the deadline for making an election was 5:00 p.m. Eastern Time on June 29, 2026 (the “Election Deadline”). The parties exp.

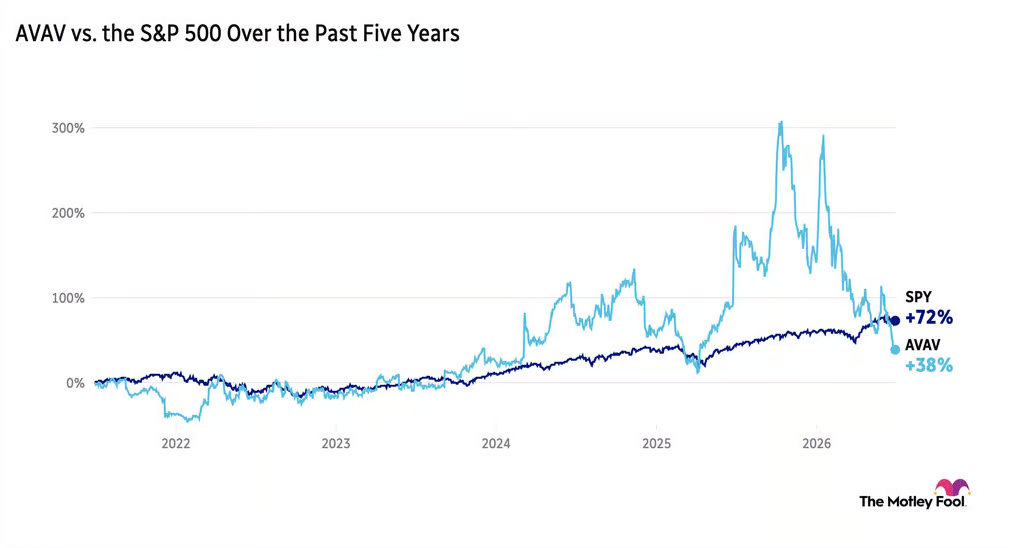

Breakfast News: AeroVironment's Best Ever Year

AVAV soars on revenue beat, investor demand drives GLW and RBLX, and more

QXO and TopBuild Stockholders Overwhelmingly Approve QXO's Acquisition of TopBuild

GREENWICH, Conn. & DAYTONA BEACH, Fla.--(BUSINESS WIRE)--QXO, Inc. (NYSE: QXO) (“QXO”) and TopBuild Corp. (NYSE: BLD) (“TopBuild”) today announced that stockholders of both companies overwhelmingly approved all proposals required for QXO to complete its acquisition of TopBuild at the companies' respective Special Meetings held today. Approximately 99% of the votes cast at QXO's Special Meeting were in favor of approving the issuance of shares of QXO common stock in connection with the transacti.

How a Yahoo! Finance Error Sent QXO Stock to $200

Small-cap and microcap reverse mergers have special risks associated with them. The incident presents an opportunity for investors to prevent future exposure to such events.

📊 AI Financial Analysis

Powered by StockMarketInfo"QXO reported Q1’26 revenue of $1.73B and net loss of $227.1M (EPS: -$0.35). Versus Q1’25, revenue increased sharply (+12,612% YoY) while net income deteriorated from +$8.8M to -$227.1M (net income declined by ~-2,701% YoY). On a QoQ basis, revenue fell from Q4’25 levels (-21.2% QoQ) and net loss widened (net income down from -$90.2M in Q4’25 to -$227.1M in Q1’26; EPS -0.17 to -0.35). Profitability remains pressured: gross margin declined from ~23.9% in Q4’25 to ~23.7% in Q1’26, while operating and net margins stayed deeply negative (net margin -13.1% in Q1’26). Operating cash flow was positive at $70.6M, but free cash flow was only $48.1M as the quarter still reflected losses. Balance sheet liquidity improved materially: cash rose to $3.05B and net debt turned net cash (-$2.20B) versus net debt in Q4’25 (+$2.11B), with total assets up to $16.66B. Shareholder returns look strong on price momentum: the stock is up +75.3% over the last 1Y (far above the 20% threshold), but it comes alongside ongoing losses. Dividend yield is shown at ~0.21%, with buybacks modest ($28.1M). Overall, sentiment appears positive despite weak earnings durability."

Revenue Growth

Revenue surged +12,612% YoY to $1.73B, but declined -21.2% QoQ from $2.19B in Q4’25—trajectory looks volatile rather than steadily improving.

Profitability

Net margin remains deeply negative at -13.1% in Q1’26 (vs -4.1% in Q4’25 and -5.1% in Q3’25). EPS deteriorated from -$0.17 (Q4’25) to -$0.35 (Q1’26). Margins are not clearly stabilizing.

Cash Flow Quality

Operating cash flow was positive ($70.6M) and free cash flow was also positive ($48.1M), but profitability is worsening and cash generation is thin relative to losses.

Leverage & Balance Sheet

Liquidity improved: cash increased to $3.05B and net debt flipped to net cash (-$2.20B). Total assets rose to $16.66B and equity increased to $10.16B, supporting resilience.

Shareholder Returns

Strong total value momentum: 1Y price change is +75.3% (well above +20%). Dividend yield is modest (~0.21%) and buybacks were limited (~$28.1M).

Analyst Sentiment & Valuation

Price target consensus is ~$30.17 vs price $25 (upside implied), but valuation multiples in the provided ratios are not very informative given persistent losses.

Disclaimer:This analysis is AI-generated for informational purposes only. Accuracy is not guaranteed and this does not constitute financial advice.

Fundamentals Overview

Beacon reported a record fourth quarter and strong annual results, exceeding many targets under their Ambition 2025 plan. Despite challenges like weather-related sales slowdowns and economic headwinds, the company demonstrated robust growth in sales and EBITDA. Looking ahead, the management expressed caution due to anticipated declines in the residential roofing market and external macroeconomic pressures, setting a mixed tone for 2025.

Growth

- Net sales grew to over $2.4 billion, up 4.5% year-over-year.

- Digital sales increased approximately 20% year-over-year.

- Greenfield locations contributed nearly $22 million to EBIT in full year 2024.

- Acquisitions contributed approximately 5% year-over-year to sales.

- Total sales for the year reached nearly $9.8 billion, a 7% growth.

Business Development

- Opened 19 greenfield locations across 12 states and two Canadian provinces.

- Completed 12 acquisitions adding 42 branches and enhancing market capabilities.

- Private label TRI-BUILT brand sales grew approximately 7%.

Financials

- Record adjusted EBITDA of $223 million for Q4.

- Operating cash flow reached $360 million, driving strong cash generation.

- Net debt leverage returned to targeted range at 2.8x.

- Share repurchase program resulted in repurchase of 2.4 million shares.

Capital & Funding

- Invested nearly $127 million in capital expenditures.

- Deployed over $1.5 billion in share buybacks since 2022.

Operations & Strategy

- Executed on the Ambition 2025 plan with a focus on operational efficiency.

- Improved sales per hour worked by approximately 6% year-on-year.

- Cost actions yielded estimated annualized savings of $45 million.

Market & Outlook

- Expect residential reroofing market demand to decrease.

- Forecast total sales per day for Q1 2025 to be down in the 3% to 5% range.

- Indications of economic headwinds such as higher interest rates and labor concerns.

Risks Or Headwinds

- Potential downturn in residential new construction.

- Labor availability issues expected to persist.

- Concerns with input costs and overall weakening sentiment in new construction.

Sentiment: CAUTIOUS

Note: This summary was synthesized by AI from the QXO Q4 2024 earnings transcript. Financial data is complex; please verify all metrics against official SEC filings before making investment decisions.

📋 Official Regulatory 10-K / 10-Q SEC Filings

Direct authenticated documentation links to audited SEC database reports for QXO.