📘 ALBANY INTERNATIONAL CORP CLASS A (AIN) — Investment Overview

🧩 Business Model Overview

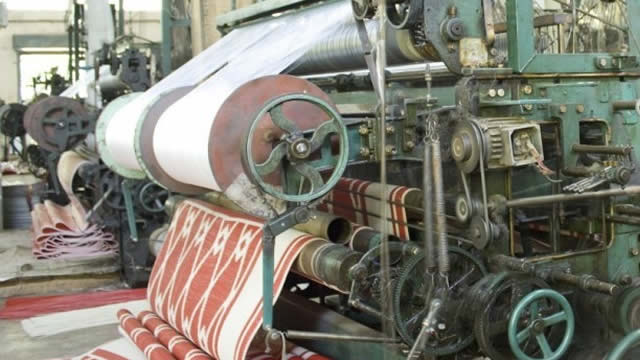

Albany International supplies highly engineered fabrics and composite materials that are embedded into customers’ industrial processes—particularly paper machines and a set of industrial/composites applications. The value chain centers on material engineering (developing the right fiber/resin architecture and surface features), converting those materials into application-specific fabrics/structures, and delivering products that must perform reliably under harsh, continuous operating conditions.

Because these materials operate as functional components of downstream equipment, customers evaluate Albany’s products on performance outcomes (throughput, runnability, downtime reduction, and end-product quality) rather than on commodity characteristics alone. This product “integration” creates customer stickiness through process validation and long service lives.

💰 Revenue Streams & Monetisation Model

Revenue is primarily product-based: engineered fabrics/clothing and engineered composite materials sold to industrial customers. Monetisation follows a mix of:

- Replacement and consumables demand tied to customer equipment operating intensity and planned maintenance cycles.

- New equipment and modernization opportunities where performance specifications drive selection.

- Multi-material performance programs where Albany’s engineered approach can support broader offerings into a customer’s installed base.

Margin drivers typically include (i) product mix toward higher-specification engineered offerings, (ii) pricing power tied to performance and reliability, (iii) manufacturing efficiency in specialty processes, and (iv) operating leverage that emerges as utilization improves in customer end-markets.

🧠 Competitive Advantages & Market Positioning

The core moat is customer stickiness from switching costs, reinforced by application-specific technical know-how and long qualification cycles in industrial settings.

- Switching costs (hard to replicate): Paper-machine and industrial process fabrics require time to qualify (runnability trials, throughput/quality verification, and reliability performance). After qualification, customers tend to stay with proven suppliers to minimize downtime risk.

- Performance engineering as an intangible advantage: Albany’s products depend on engineered material architectures and surface characteristics that affect measurable operating results, making “like-for-like” substitution difficult.

- Installed-base penetration: Even when broader industrial demand cycles, the installed base creates recurring replacement demand and opportunities during rebuilds/modernizations.

COMPETITIVE BENCHMARKING

Albany competes in specialized engineered materials rather than broad commodity manufacturing. Key competitors by end-market include:

- Voith and Andritz (paper industry OEM/component ecosystems): These companies can integrate solutions around paper machinery and associated components, creating a system-level offering advantage.

- Kadant (industrial equipment and selected process components for paper): Often competes through equipment adjacency and installed-base relationships.

- Hexcel / Toray (composites and advanced materials in adjacent applications): Strong positions in certain composites segments create competition where material performance specifications overlap.

Industry focus contrast: Albany’s differentiating emphasis is on engineered fabric and composite materials designed for demanding process roles. In contrast, large OEMs (Voith/Andritz) may compete via equipment/system integration, and composites leaders (Hexcel/Toray) compete where material platforms dominate—Albany competes by combining performance outcomes with fabric/material engineering tailored to specific operating environments.

🚀 Multi-Year Growth Drivers

A multi-year thesis is anchored in durable end-market needs and ongoing modernization:

- Process efficiency and quality improvements: Customers seek higher uptime, better product quality, and reduced operating costs—conditions that reward engineered performance materials.

- Modernization of industrial assets: Equipment refresh cycles support incremental demand for engineered fabrics/materials where performance and reliability specifications tighten over time.

- Expansion of engineered offerings: Scaling higher-spec products and application-level engineering capabilities can expand addressable opportunities within existing customers’ installed bases.

- Industrial diversification: Growth opportunities in adjacent engineered-material applications can partially offset cyclicality in paper-related end demand.

Over a 5–10 year horizon, TAM expansion is less about new “one-off” projects and more about deepening penetration of engineered solutions into a large installed industrial base.

⚠ Risk Factors to Monitor

- Industrial demand cyclicality: Paper and industrial production levels influence replacement volumes and modernization budgets.

- Customer qualification and supply chain complexity: Specialty materials can face transition risks; delays in customer acceptance or execution issues can affect growth.

- Competition and pricing pressure: OEM-adjacent competitors can bundle solutions, and in some end-markets buyers may seek lower-cost alternatives.

- Capital intensity and manufacturing execution: Specialty manufacturing requires disciplined capex and process control to sustain quality, yield, and cost competitiveness.

- Customer concentration: Any meaningful shift in a small number of large customers’ spend patterns can impact segment-level results.

📊 Valuation & Market View

The market typically values engineered industrial suppliers using earnings power and cash generation, often reflected through multiples such as EV/EBITDA or P/E depending on the investor base. Valuation sensitivity tends to concentrate on:

- Structural margin profile: The durability of specialty mix versus commodity-like manufacturing.

- Evidence of pricing and mix discipline: Ability to pass performance-related value into pricing.

- Utilization and operating leverage: How reliably margins hold through end-market cycles.

- Industrial diversification progress: Reducing reliance on any single application end-market.

Because this business sits in cyclical industrial end markets, the market’s “right” valuation often depends on perceived resilience of the installed-base economics (replacement demand and qualification stickiness) versus cyclical drawdowns.

🔍 Investment Takeaway

Albany International’s long-term attractiveness rests on a structural moat driven by switching costs and performance qualification in industrial process materials. The company’s ability to compete through engineering-driven, application-specific solutions supports installed-base replacement economics and modernization participation, offering a relatively durable earnings model compared with commodity materials producers—while still requiring active monitoring of industrial cyclicality, competitive pricing dynamics, and execution in specialty manufacturing.

⚠ AI-generated — informational only. Validate using filings before investing.